.){kind=link}

In this article, a trading system with a very simple logic will be developed, which, as will be seen, can be applied to different cryptocurrencies with truly interesting results. The system is based on the Average True Range, which is used as a volatility indicator, and in this specific case, it will be applied to Bitcoin (BTC). Recently, the queen of cryptocurrencies has been much talked about, both for the anticipation of an important rally following the latest Halving and for its growing role as a strategic asset as a store of value against the inflation typical of fiat currencies.

Summary

How the Average True Range Volatility Indicator Works

The Average True Range (ATR), or “the average true range,” is a technical indicator used to measure the volatility of an underlying asset over a specific time period. It was developed in 1978 by Welles Wilder Jr, a renowned commodities analyst. The main objective of the ATR is to provide a numerical indication of the volatility of a particular instrument or market.

A high ATR, in fact, indicates a market with high volatility, while a low ATR expresses greater stability in the price of the underlying and, therefore, a lower risk profile.

This indicator expresses the price variation of a financial instrument over a specific time period, but it is not able to provide information regarding the market direction and its momentum.

As the name suggests, to calculate the ATR it is necessary to measure the average of the “true range” which, unlike the simple “range” (that is, the maximum value minus the minimum of a bar) is defined by also considering any gaps with respect to the closing of the previous bar.

Generally, the measurement is carried out for 14 periods, but the ATR can also be calculated over different intervals depending on the needs of the trader.

The trend following strategy on Bitcoin: logic and trading backtest

The strategy in question is a simple upward trend following, designed for the spot market but also applicable to futures, which will enter the market with a stop order at the break of a certain price level, with the idea that the ongoing movement may continue upward.

The session under consideration conventionally runs from 00:00 GMT to 23:59 GMT. Since cryptocurrencies are quoted 24 hours a day, these times have been chosen to align the session with the solar day. A 15-minute bar ‘time frame’ will also be used to operate rather precisely in the market, but also using a second data series (data2) with daily bars for calculating the entry level.

This, in fact, will be determined by the closing of the last daily bar plus a certain amount, determined through the Average True Range (ATR) of the last 5 days (period), then multiplied by a factor (factor) which will initially be set equal to 1.

compra la prossima barra a c data2 + factor*AvgTrueRange(period)data2 stop;

Assuming to operate with $10,000 per operation, the closure of the trade will occur upon reaching a stop loss of $1,000, a rather large value but assumed necessary in this market, given the volatility of Bitcoin and how it is nervous in its movements. In any case, the strategy has an intraday horizon, so it will close positions by the end of the session, without the need to use a take profit.

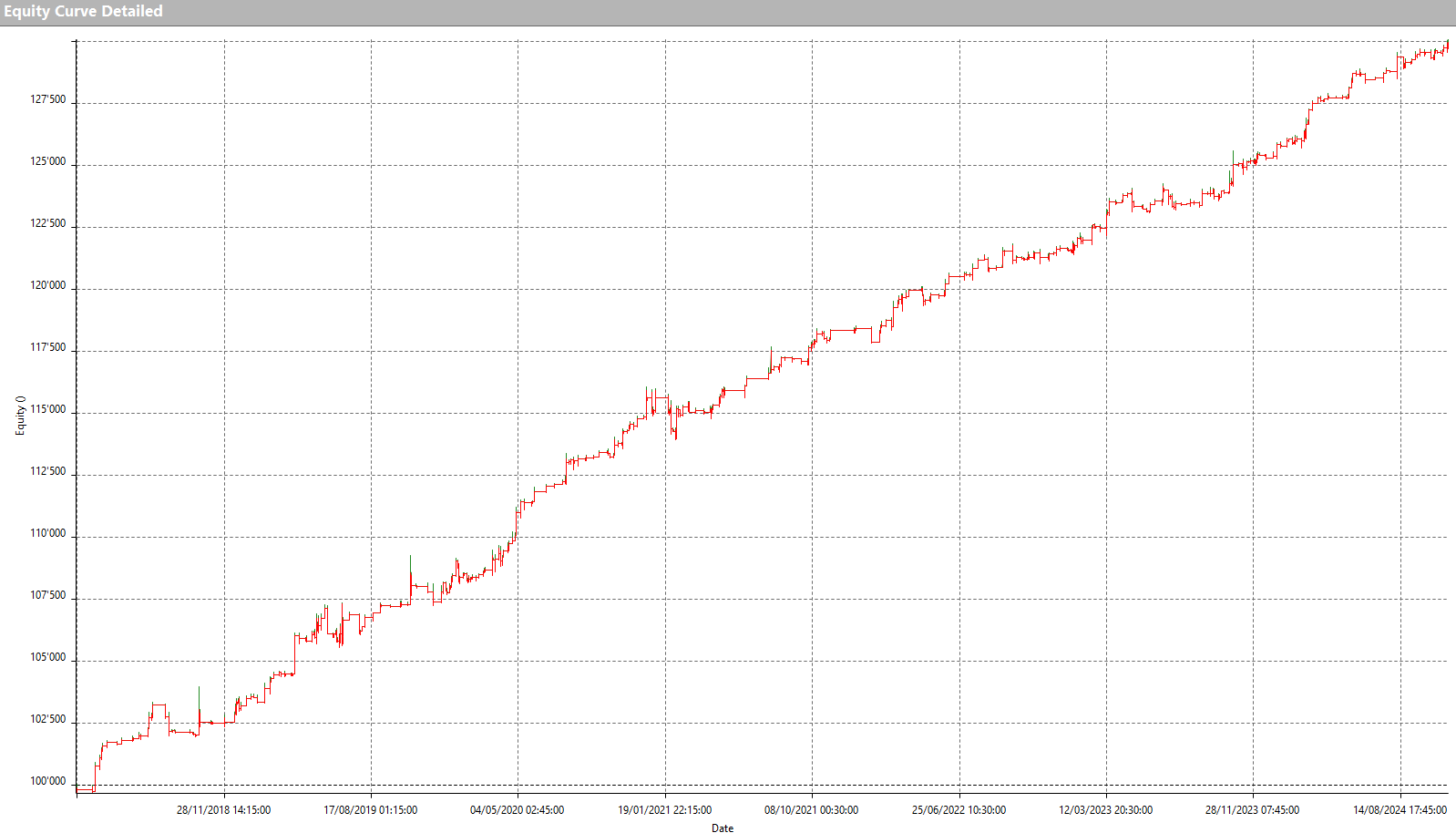

By applying this strategy to the Bitcoin spot market (BTC) against USDT (stablecoin pegged to the dollar), from January 2017 to October 2024, very encouraging results are obtained, with an equity line that rises quite steadily.

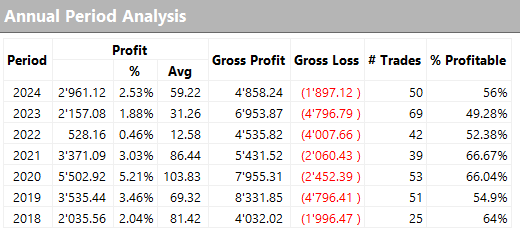

This is confirmed by the annual results reported in Figure 2, which, however, denote an average trade that is not very high, which could therefore be improved to make the strategy more robust with a view to also supporting the operational costs of real trading (commissions and slippage in order execution).

How to optimize the performance of the trend following strategy on Bitcoin

Among the variables that can be adjusted to optimize the strategy, there is certainly the period (period) used to calculate the ATR, but also its multiplicative factor (factor) and the stop loss value.

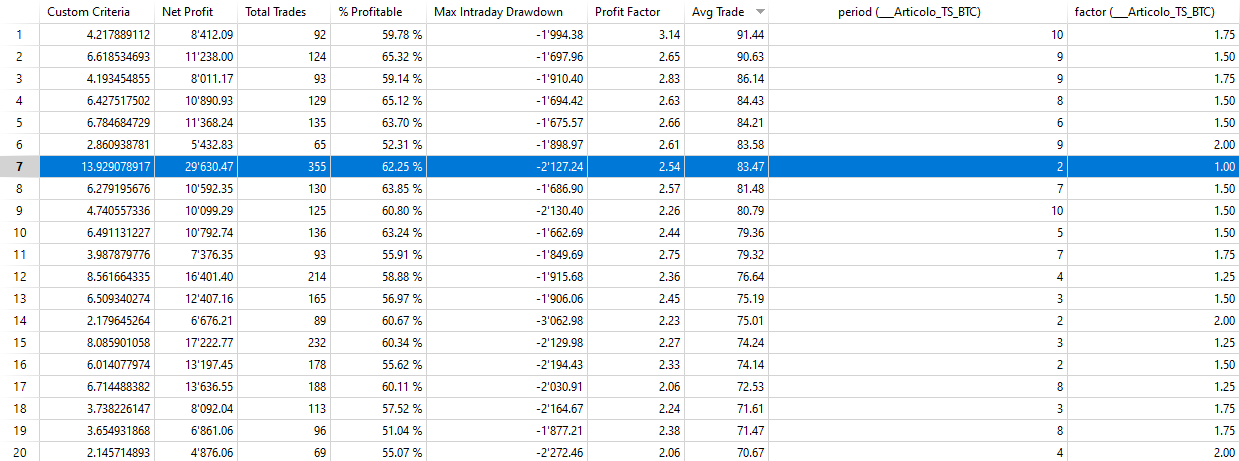

By varying the ‘period’ between 2 and 10 days and the ‘factor’ between 0.5 and 2 (with a step of 0.25), while keeping the stop loss unchanged for the moment, the results shown in Figure 3 are obtained.

Ordering them by average trade, it is noted how the combination ‘period’=2 and ‘factor’=1 allows for an excellent net profit/drawdown ratio (the Custom Criteria) and the best net profit (about $29,600) among those with the highest average trade. In fact, there are also combinations with higher net profits, but with average trades too low to be considered.

With the selected parameters, therefore, the total profit of the system approaches $30,000 in 355 trades, with an average trade of about $83.50. These results indicate a strategy already quite good to be applied in live trading, but that does not mean that it cannot be worked on to improve it further.

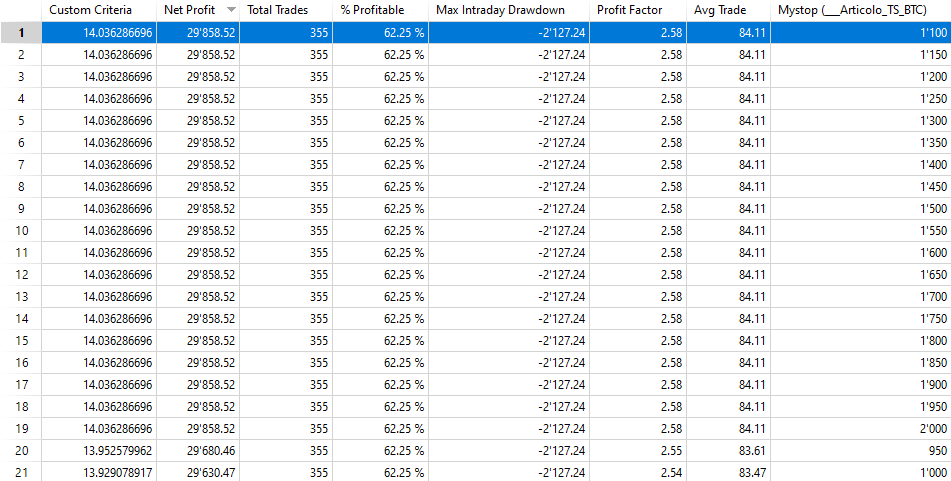

At the moment, in fact, the strategy involves the use of a stop loss at $1,000, which is 10% of the position’s value, and it has not been optimized. In Figure 4, it is noted that by varying the stop loss from $500 to $2,000, there are no particularly interesting results, so one could maintain the initial stop or at most take the value of $1,100, which turns out to be the optimal one.

Trend following strategy: application to other cryptocurrencies (Ethereum and Solana)

Without going further by inserting operational filters that could easily lead to overfitting in the optimization of the strategy, one could simply try to validate it by applying the same logic to other cryptocurrencies, to verify if it can also achieve good results on these. It is known, in fact, how Bitcoin acts somewhat as a driver for the entire market, so the other cryptocurrencies tend to move in a similar manner.

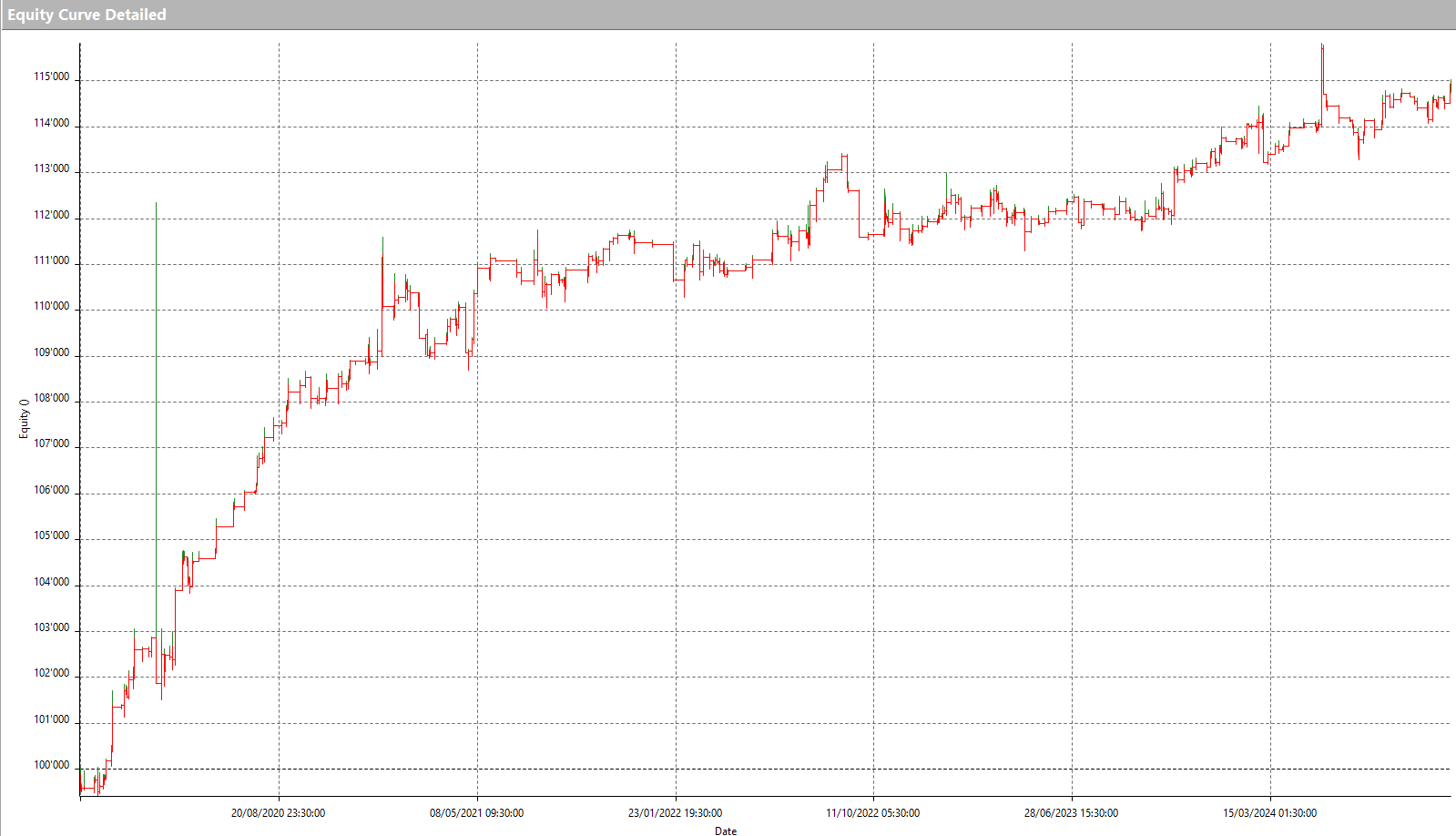

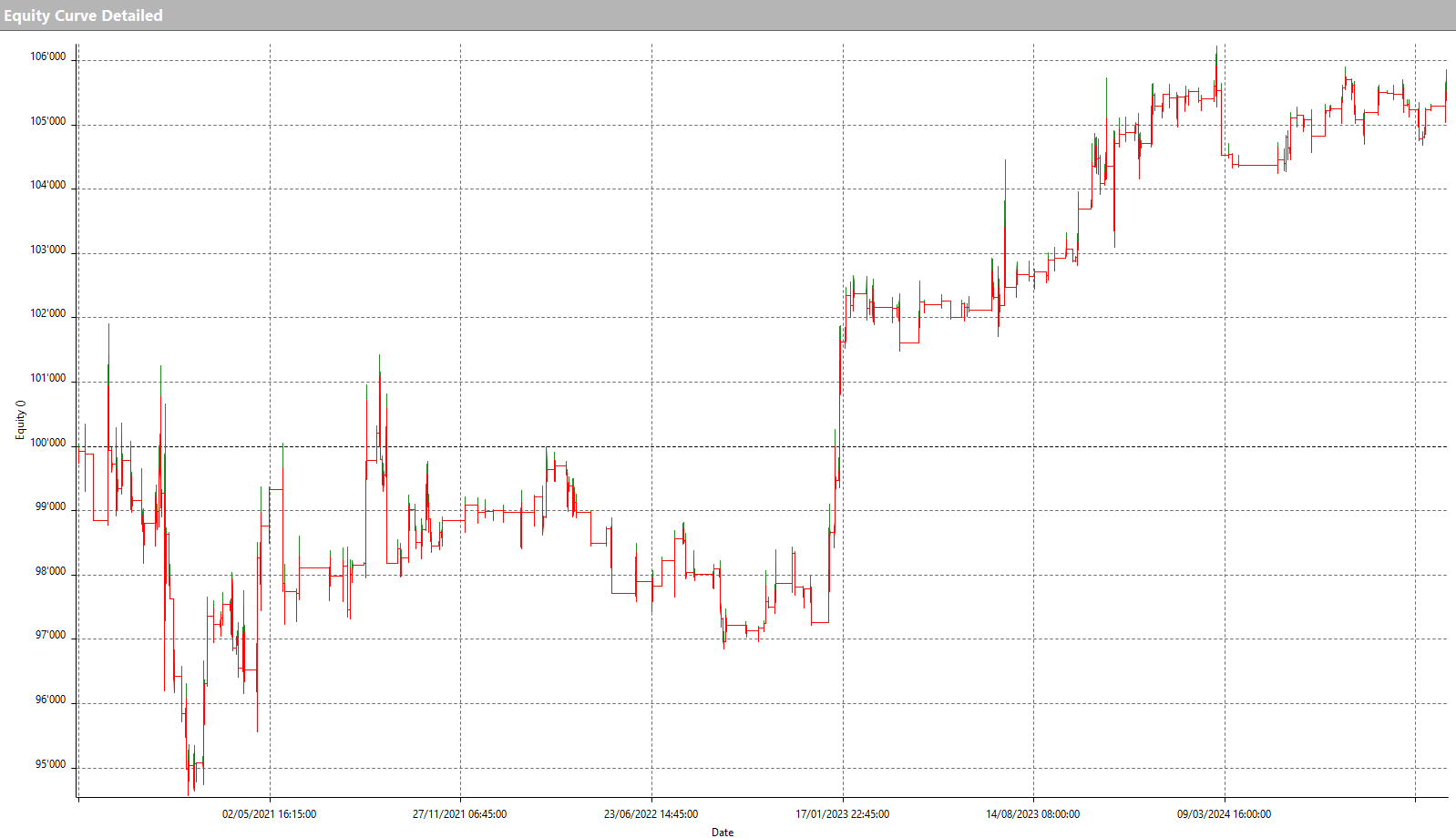

The equity lines of the same strategy applied to Ethereum (ETH) and Solana (SOL), two of the main altcoins on the market, are reported below.

The upward trend of both equity lines confirms the effectiveness of the strategy, although to achieve the best results from Ethereum and Solana as well, it would be necessary to proceed with the optimization of the parameters, as previously done for Bitcoin. This task is therefore left to the reader as an operational suggestion.

Conclusions on the strategy that exploits the volatility of Bitcoin and cryptocurrencies in trading

In conclusion, the intraday trend following strategy tested on Bitcoin has proven to be certainly interesting in its simplicity, and it can be applied with the necessary adjustments and optimizations to many other cryptocurrencies as well. This market is indeed still quite young, and despite maturing rapidly, it presents numerous opportunities for traders who wish to engage with it.

Until next time and happy trading!

Andrea Unger