In this new article, we are going to look for recurring behavior on Bitcoin, the largest cryptocurrency by capitalization within the crypto landscape, to maximize trading profits.

Specifically, one will go looking for the best time within the session to trade in favor of trending. Hourly bars will be used, with width equal to 60 minutes, and “buy stop” orders will be placed on the high of the previous bar.

Trading: best times for a trend following strategy on Bitcoin

Unfortunately, as of today it is not yet possible for Italian traders to use cryptocurrency futures, which is why the strategy will be built on the spot market. The mode will be “long-only,” so the strategy will only carry out trades to the upside, since it is very complex to short on the spot market automatically.

The fixed monetary position used is $100,000, a purely symbolic figure because obviously spot Bitcoin is a very scalable market and it would be possible to trade even with positions of less than $1,000 in monetary value. The tests were run from January 2019 to the most recent days (July 2023).

Prior to 2019, Bitcoin was a different market than it is today, with much lower liquidity. In addition, pre-2019 data is often corrupted, or somewhat less reliable, as it has fictitious gaps or spikes not actually recorded by the market.

Clearly all of this can have a negative impact on the performance of the strategy and the robustness of the chosen filters. We will therefore limit the backtest to the last 4½ years, so that we can work with data that is as reliable as possible.

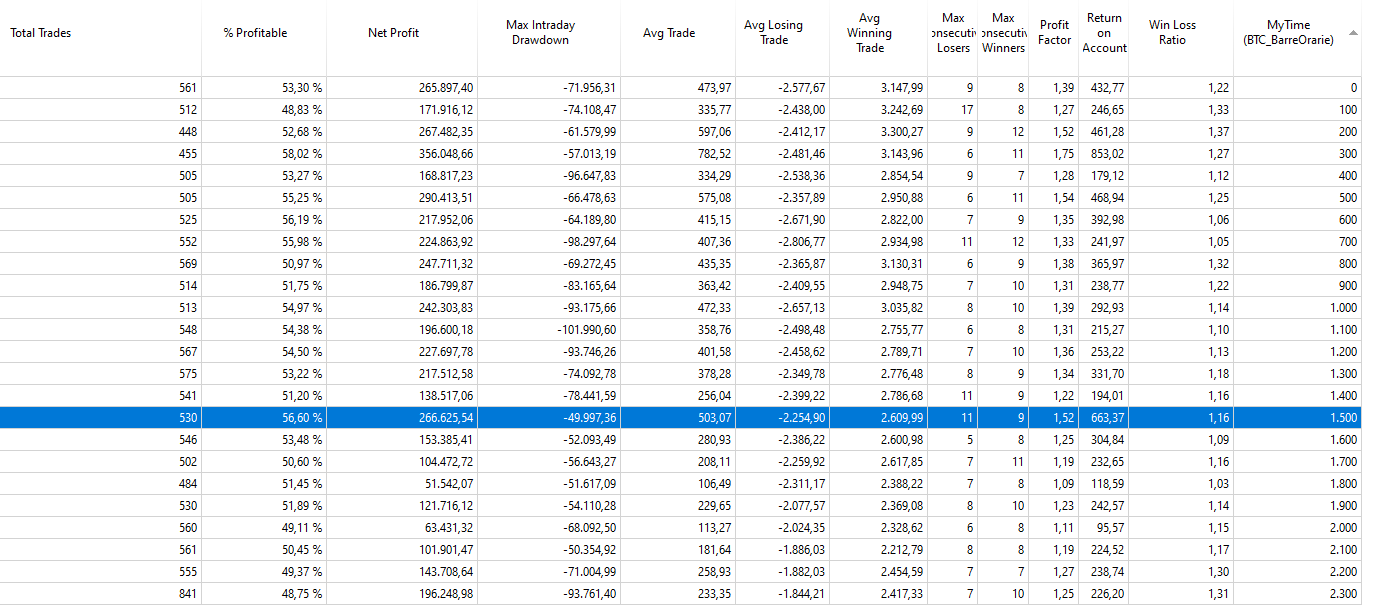

In Figure 1, it can be seen from the entry time optimization that the propitious time to place stop orders on the high of the previous bar is 3:00 PM (CET). Good results are concentrated around this value and, not coincidentally, this time coincides with the opening of Wall Street, which is known to trigger volatility in the markets, including Bitcoin.

Values between 7:00 AM and 10:00 AM (CET) also seem potentially advantageous, which are times when European traders begin to trade Bitcoin, just as is the case between 2:00 AM and 3:00 AM where Asian traders are the ones to lead the way. In this case, 3:00 PM was chosen because of a more limited drawdown than in the aforementioned cases and to favor the US session, which is generally more volatile and more interesting to look for breakouts.

Backtesting of the strategy used, with variations

The strategy will close its positions on the day following the trade opening date. At this point in the development, the stop loss, a key parameter in creating a strategy, is still missing, but will be added shortly.

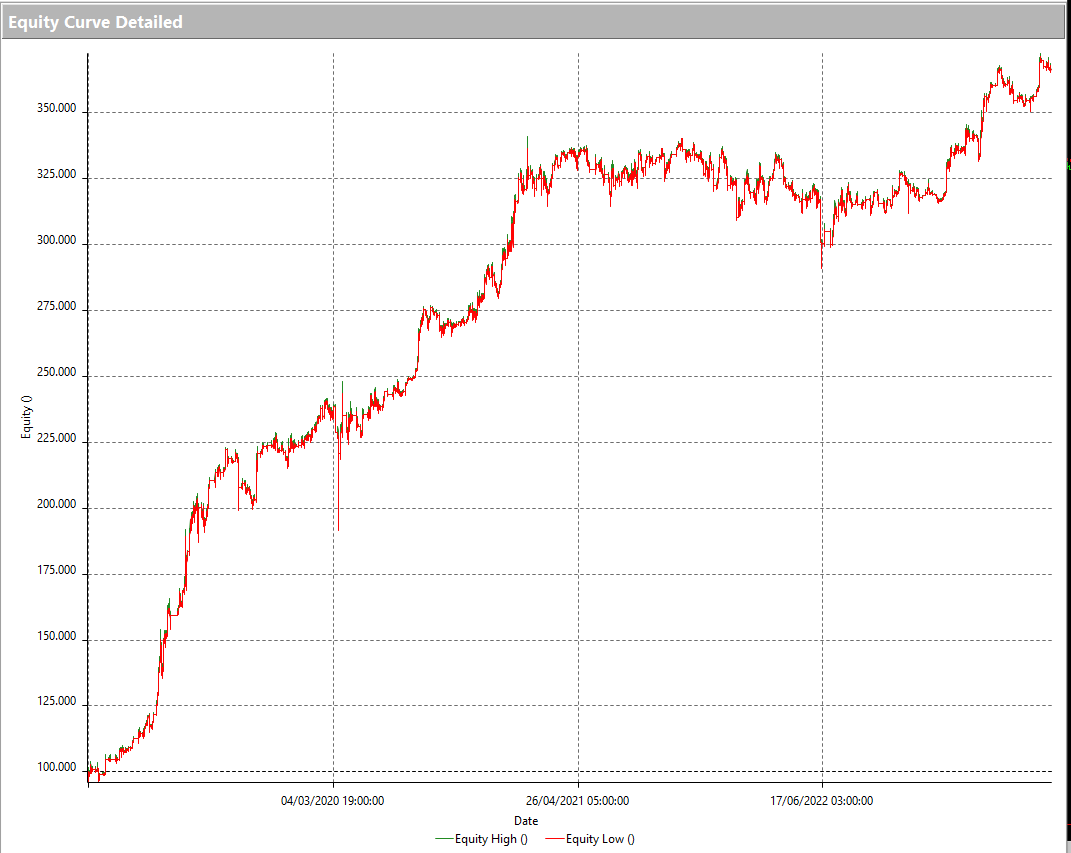

The results of the system, visible in Figure 2, 3 and 4 are encouraging from the start. The equity line is positive, with a few shocks experienced between 2021 and 2022. It is worth noting that in those years it was almost impossible to identify a good time to buy, given the strong drawdowns experienced by the market (about -70% from historical highs).

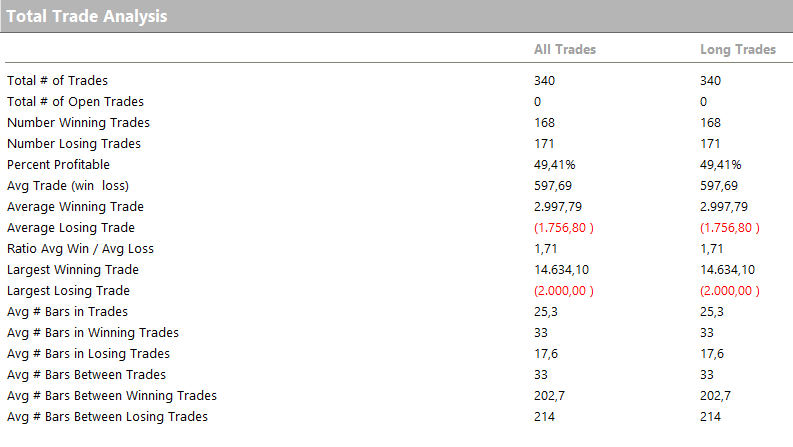

The average trade comes to $500, which is 0.5% of the value of the average position taken by the strategy ($100,000), a value that is certainly acceptable and that is able to cover the commission costs and the possible slippage that one would face through the live use of this strategy.

At this point, we proceed to add a stop loss with the goal of reducing the system drawdown and cutting losses where the open trade does not look too promising.

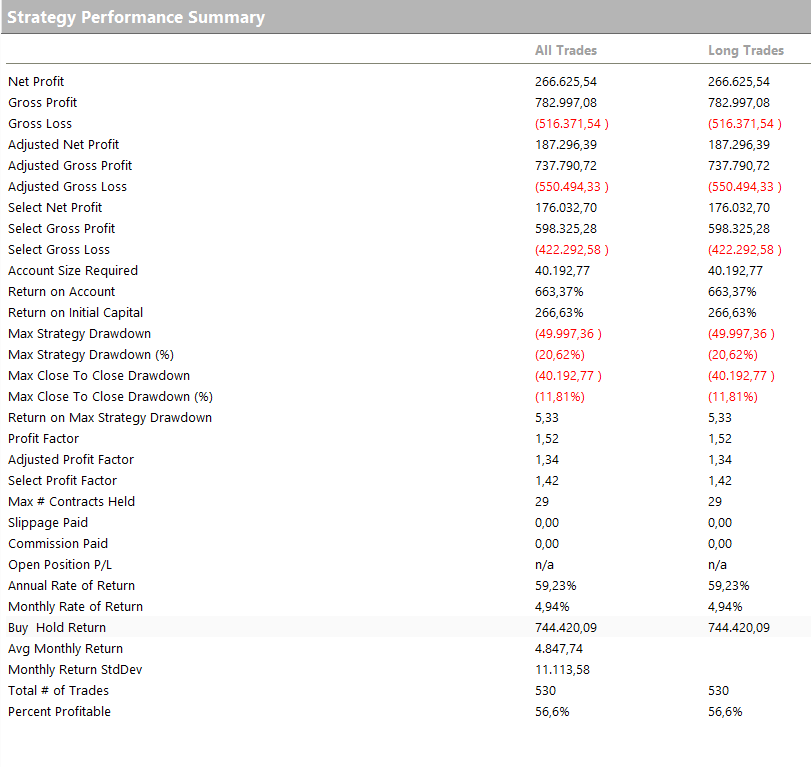

Figure 5 shows how a stop loss at $2,000 (2% of $100,000) improves the system by cutting the drawdown from -$50,000 to about -$30,000. The equity line (Figure 6) also seems to no longer suffer as much from the drawdown experienced by Bitcoin between the end of 2021 and 2022, an indication that indeed the stop loss acts as protection from excessive losses.

Although this is a good result, further investigation is required as we see the average trade drop from the previous $500 to about $400 now.

One of the problems is that the strategy at this point of development still executes a lot of trades, more than 100 per year on average, given the last 4 1/2 years. Hence, it is necessary to filter this volume of trades through specific conditions that identify the best times to buy Bitcoin.

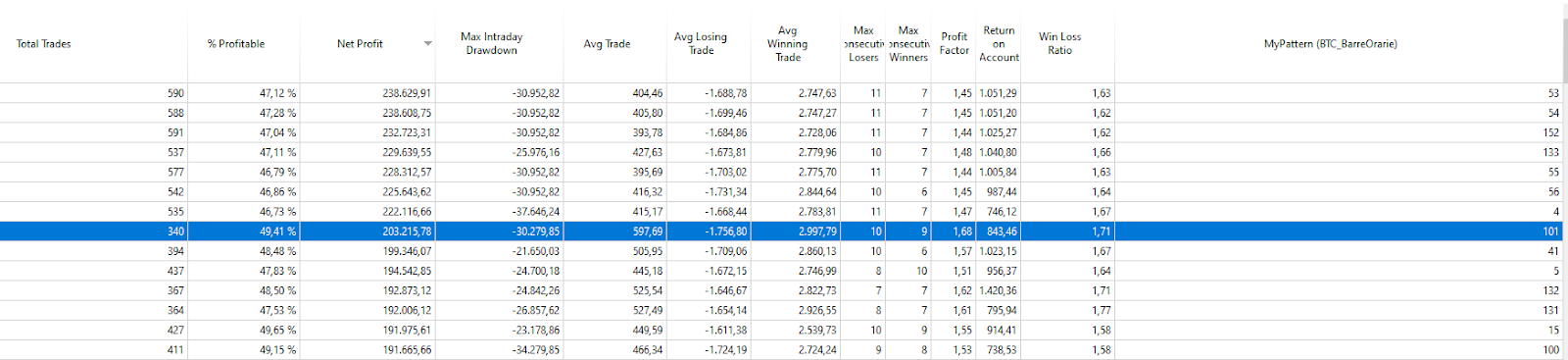

Figure 7 shows how by optimizing a list of proprietary patterns encompassing 152 different combinations, Pattern 101 increases the average trade from the previous $400 to about $600. A significant improvement in strategy performance.

The Pattern 101 in this list is to trade only if today’s session low is at least 0.5% higher than the previous session low. It seems that buying on weakness leads nowhere; in fact it should be avoided. Instead, the net profit is minimally affected by this addition going from the intial $230,000 to $203,000, but this is to the benefit of the average trade, which denotes that the quality of the trades has increased, and it matters little if you leave a small amount of profit on the plate.

At this point in the development, the results are comforting. The equity line, especially in the most recent period, shows good consistency. The average trade, as explained earlier, is also acceptable and would allow one to cover the commission costs and slippage one would face by trading live on the Bitcoin spot market.

This market has once again proven to be trend following, capable of staying in trend for multiple days and continuing in the direction taken even after a breakout. However, in this particular case it was the addition of the stop loss and Pattern that provided the most significant improvements to this strategy.

Hopefully, the article has been helpful, particularly in understanding the dynamics governing Bitcoin and its main characteristics.

Until next time!

Andrea Unger

{kind=link}