The total value locked on liquid staking crypto protocols is rising on Solana’s blockchain: the trend is expanding outside Ethereum as well.

As a result of the Shapella update and the integration of LST tokens within DeFi, this niche market has been wildly successful, culminating in contagion on Solana.

Let’s take a look at all the details together.

Summary

Solana crypto: liquid staking platform activity on the rise

The trend of liquid staking crypto platforms has also arrived on Solana, leading to an uptick in TVL for this kind of protocol.

Particularly in the first half of 2023, we have seen a substantial increase in total value locked, sparking particular interest from the decentralized finance audience.

Liquid staking applications allow users to take advantage of returns offered by staking platforms (such as Ethereum 2.0) while taking advantage of alternative liquidity, known as LST tokens.

This mechanism has been highly appreciated by users in the Solana ecosystem, who have deposited about $89 million since the beginning of the year as a result, marking a 91% increase.

In total, about 1.66 million SOL have been blocked, corresponding to $31 million, plus a whole range of tokens involved in liqudity providing processes such as USDT, USDC, wLDO, stSOL and WETH.

It is very interesting to note that of the 270 million TVL allocated on ALL protocols in the Solana network, 69% of this amount is locked precisely into liquid staking protocols.

Kevin Peng, research analyst at blockchain analytics firm The Block believes that the Shapella update in April, which allowed the unstake of previously deposited ETH on the Beacon Chain, has been a catalyst for the growth of the entire industry.

These are his words:

“Overall, LSDs have grown as a category across crypto in 2023 in large part due to the new dynamics around staking on Ethereum, though demand for these products has trickled into the Solana ecosystem as well.”

The best liquid staking dApps on Solana and Ethereum

Let’s now analyze in detail which liquid staking crypto platforms are the most in vogue on the Solana and Ethereum ecosystems.

Starting with Solana, we can easily observe that Marinade Finance, according to data from DefiLlama, represents the most used protocol in the community with $125 million in TVL, representing a total market share of 62%.

Next we find Lido, which with $55 million manages 27% of the capital placed in this niche.

Then in lesser presence are Jito, JPool and Socean, which collectively encompass $24.9 million.

As for Marinade Finance, it is curious to note that despite the strength expressed on the Solana network, it has lost a great deal of capital since November 2021, where the TVL was $1.8 billion.

The onset of the bear market, and later the collapse of FTX, decreed a downsizing of this protocol and the entire ecosystem of DeFi applications on Solana.

On Ethereum the situation is different: while we see low activity in decentralized finance compared to the values recorded at the height of the bear market, we can see how liquid staking platforms have grown quite a bit in recent months.

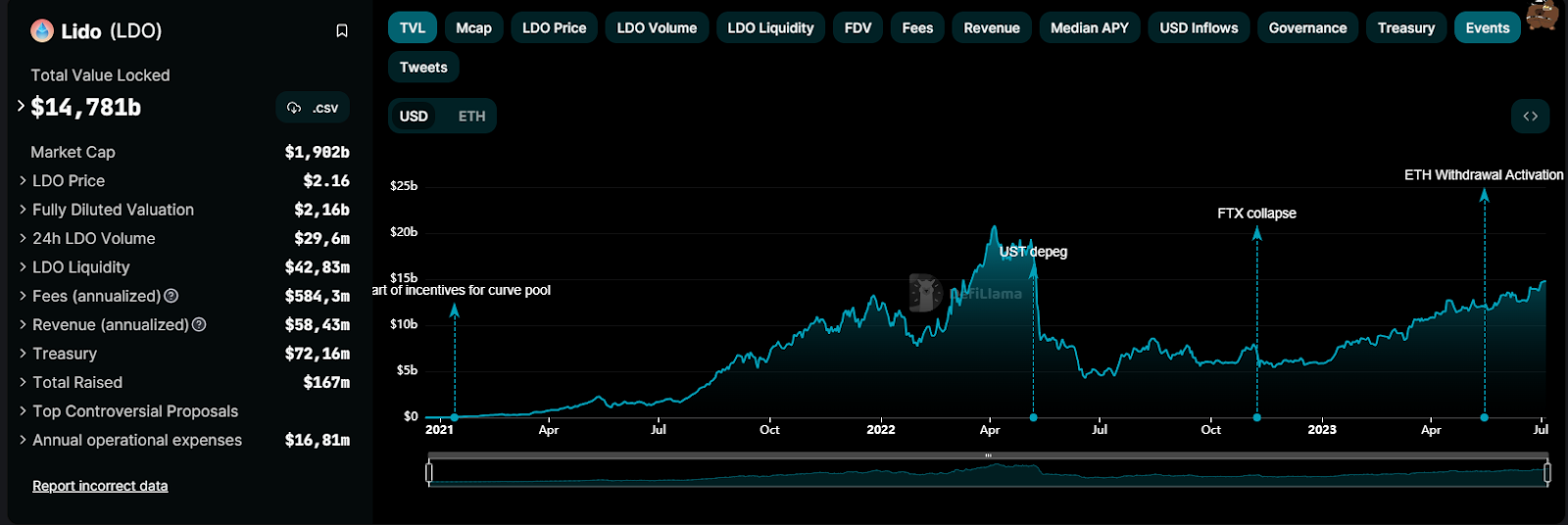

Lido on Ethereum concentrates most of its firepower, where it represents DeFi’s largest decentralized application, with a TVL of as much as $14.7 billion.

As of early 2023 there has been impressive growth for this protocol, which as anticipated earlier, has benefited from the unstake of ETH from the Beacon Chain.

The other most used LSD platforms on Vitalik Buterin‘s chain are Coinbase wrapped staking with $2.2 billion, Rocket Pool with $1.9 billion, Frax with $453 million, Stakewise with $177 million, and Ankr with $93 million.

It is worth noting how all these applications do not exceed the numbers recorded by Lido overall, which remains the undisputed leader in the industry, with high growth prospects for the coming months.

Integration of liquid staking tokens into DeFi

The use of liquid staking platforms has become very intense since the beginning of this year, partly due to the integration that has emerged between LST tokens and the main DeFi platforms.

Until recently, in fact, those who deposited assets in these protocols could only use the liquidity provided to them to trade on decentralized markets or to be transferred to exchanges.

Now, however, thanks to the creation of several liquidity pools in DeFi and the integration of this token with lending platforms, the attractiveness to this kind of financial product has become significantly higher.

According to Glassnode‘s data, this is a key value proposition for LS tokens, which have found a very attractive match for investors, who can leverage their liquidity while getting returns for staking.

Take lending pools such as Aave and Compound as an example: the Aave stETH/wstETH pool has grown by leaps and bounds since the beginning of the year, with total current liquidity at $2.53 billion.

Investors have appreciated the ability to borrow coins by providing the same liquid token received from Lido as collateral.

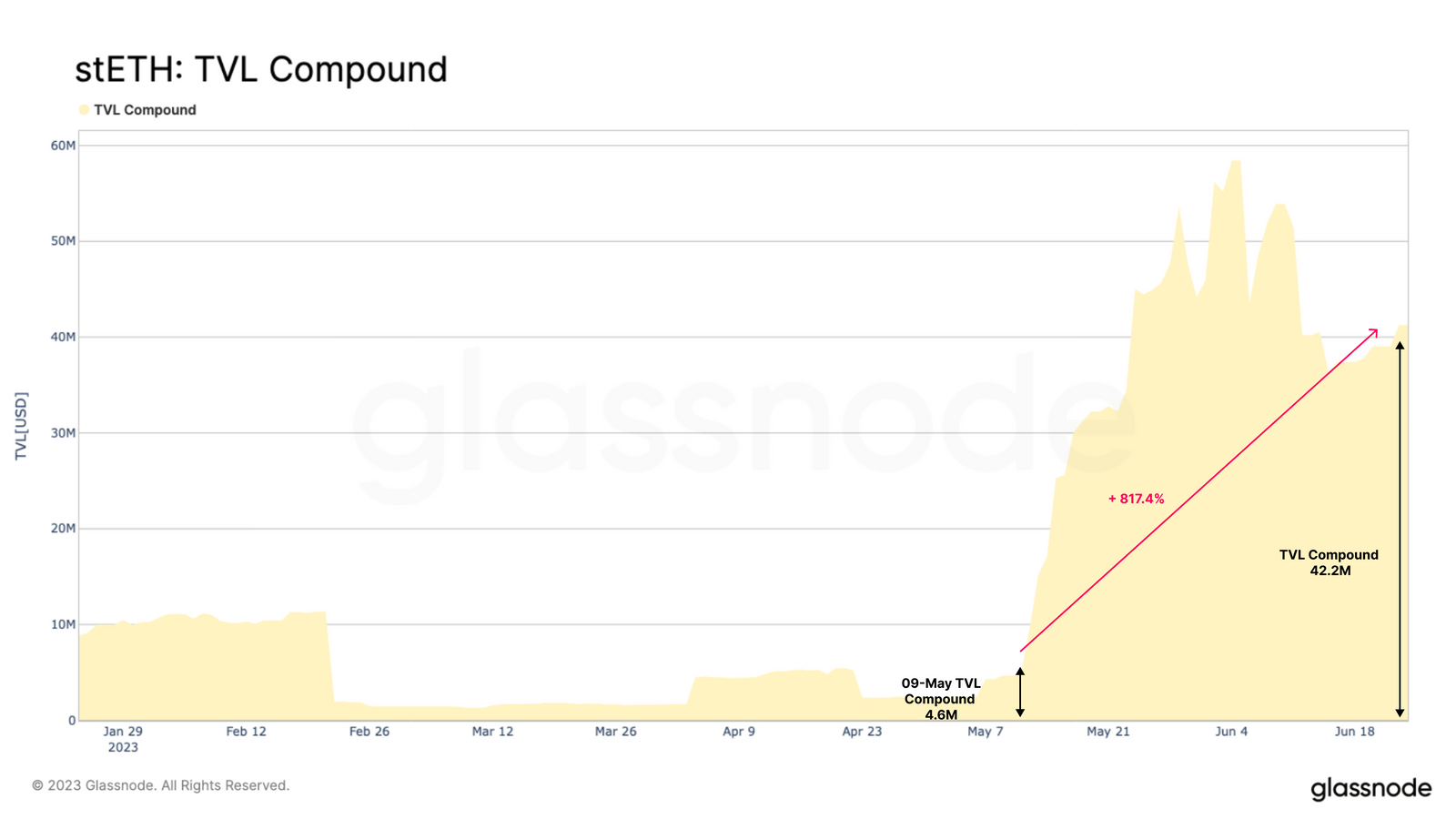

We can also observe the same trend on Compound: the wstETH pool as of May has experienced an impressive growth of 817%, now holding about $42.2 million in counter value.

It seems that LST derivatives are becoming more attractive in the DeFi arena not only than the more capitalized cryptocurrencies such as ETH and WBTC, but also than stablecoins, historically the most widely used in these contexts.

{kind=link}